Search

Search

www.google.com

www.google.com

Choosing the Right Account(s) for You Article

Once you have chosen a financial institution, you need to decide what account or combination of accounts will meet your needs. Before you choose your account(s), think about what you want to do with your money.

Most financial institutions offer 2 main kinds of accounts: Chequing accounts and Savings accounts.

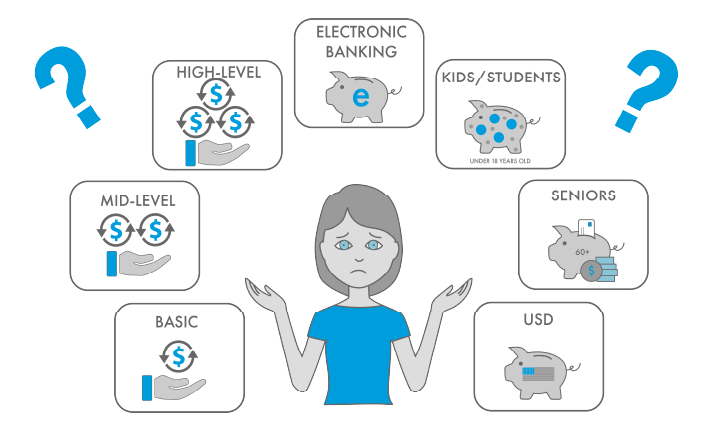

Chequing Accounts

Chequing accounts are not just about the ability to write cheques. In fact, in today’s world, you may have a chequing account and not even have cheques for your account as there are so many other ways to make withdrawals. The term chequing account usually refers to an account that you use as an everyday account. One that offers you the ability to make regular withdrawals but doesn’t usually earn much or any interest. Generally, this is the kind of account where you will deposit your paycheque and pay your bills. You may have a debit card attached to this account so you can make purchases in stores and withdraw money at an ATM.

Financial Institutions usually offer a variety of chequing accounts with different features and fees. Take the time to look at the different options and fees and compare that to your spending habits to ensure you choose the right account for you.

Most Financial Institutions offer several different types of chequing accounts. Generally, they will offer at least a basic, mid-level and high-level chequing account option. Often the basic level is what is known as a pay-as-you-go account. This will have a low monthly fee or maybe even no monthly fee. However, these accounts don’t usually include any free transactions so you will pay for each transaction. If you don’t have a lot of bills or won’t be using your account much, it may be the best option for you. However, if you tend to have moderate to high levels of spending in a month, you will likely be better off looking at an account with a higher monthly fee but with free transactions included in that monthly fee.

Some financial institutions may offer accounts with age-based discounts such as a student account with lower fees or a senior’s account with some additional discounts. Some will have accounts designed to cater to a specific kind of banking personality. For example, if you prefer to do most of your banking online or on your smartphone, you may want to check if your Financial Institution has an account that provides discounts for self-serve/electronic banking options and charges a little more for in-branch transactions.

If you are unsure what chequing account will suit you best, be sure to talk with someone at your financial institution. If you can tell them how you plan to use your account, they should be able to guide you to the best account for you.

As you move through life, you may also find that your spending habits change and so it’s a good idea to take a look at your chequing account every once in a while to ensure that your account is still the best account for you. You may find that you need to change your account and your bank or credit union will be able to help you do that.

Savings Accounts

Savings accounts are accounts that allow you to save money and earn interest. Before you choose a savings account, it’s a good idea to think about your long and short term savings goals and how you plan to use your account. Most savings accounts do not charge a monthly fee and so you will need to consider other factors when you make your decision.

Some things to consider are:

Number of Free Withdrawals/Transactions: Some savings accounts will offer a couple free withdrawals or transactions per month but will charge you for any transactions over that number and some may charge for all transactions. Others may waive transaction fees if you keep a minimum monthly balance in your account. Consider how many withdrawals you plan to make and how often you expect to make them and compare that with your savings account options.

Interest: Savings accounts are generally defined by the ability to earn interest but they do not all have an equal approach to how they calculate and pay interest. Here are some things to consider:

A. Interest Rate: Start by looking at an account’s posted interest rate. How much does the account say you will earn and how does it compare with your other options. Some accounts may offer a special higher introductory rate for a limited time to entice you to open that account but after the introductory period is over, they will revert to a much lower interest rate. Be sure you know what rate you will receive long term and how it compares with your other options.

B. Interest Rate Calculation: It’s important to look at how interest on your savings account is calculated and paid. A daily interest account is calculated on the balance of your account every day and is usually paid at the end of the month. Monthly interest is calculated based on your lowest account balance during the month and then paid into your account at the end of the month. Similarly, quarterly interest is calculated on your lowest account balance during that quarter and paid into your account at the end of the quarter. And, annual interest is calculated on your lowest account balance over the year and then paid out at the end of the year. As a general rule of thumb, the longer the interest calculation period, the higher the interest rate.

Most savings accounts operate on a principle of compound interest which is a way of calculating interest where you earn interest on your interest. So, when you deposit money into your savings account, you will earn interest on the amount you deposited (which is called the principal). The interest you earn is deposited into your account and then for the next interest period, the interest you earned will also be included in your savings account total and so you will earn interest on your principal and the interest that you earned in the last interest period. As long as you leave that interest in your account, you will continue to earn interest on your interest and it will continue to compound and grow. And, of course, the longer you continue to save your money, the more compound interest you will earn and the faster your savings will grow.

C. Minimum Balance: Some savings accounts will require that you maintain a minimum balance in your account to earn interest. So, for example, if the minimum balance requirement is $1000, you will not earn interest on your savings account unless you have at least $1000 in your account. Some financial institutions will pay you interest on the full $1000 when you reach that minimum balance and others will only pay interest on the amount that exceeds $1000. Keep this in mind when you choose a savings account. If you will not be able to maintain that minimum balance, then you may not earn any interest at all on your savings.

D. Tiered Interest: Similar to the minimum balance above, some savings accounts will be based on a tiered interest scale. For these accounts, the financial institution will set up a tiered system based on your account balance to determine how much interest you earn. So, for example, you may earn no interest on an account balance of $0 to $4999.99 and then 1% interest on an account balance of $5000 to $9999.99 and then 1.5% interest on account balances of $10,000 and more. It’s important to understand how your bank calculates the interest. Even if you have $8,000 in your account, you will not necessarily earn any interest on the full $8000 but rather will earn no interest on the first $4999.99 and will earn 1% interest only on the portion that is ‘in’ the 2nd tier.

C. Minimum Deposit: Aside from requiring a minimum balance for interest, some savings accounts might require a minimum initial deposit to open them.

When you’re choosing an account, don’t get stuck trying to choose between a chequing account or a savings account… the right decision may be for you to open one of each. Consider your finances, your spending and savings habits, and your long and short term goals when choosing an account. If you need help deciding, reach out to someone at your financial institution and they should be able to guide you in your decision making process.